When looking to start or fund a business in Ontario, a company must often evaluate the different methods available to it for obtaining financing. The ultimate choice will depend on factors such as the structure and purpose of the business, its specific monetary needs, and its current size and goals for future growth.

There are several ways for a business to obtain “traditional” financing, with banks, trust companies and credit unions being the most common and accessible lenders. Specialty lenders in Canada can also provide financial assistance through mortgage, leasing, factoring, floorplan or other asset-based loan programs. Some businesses, especially start-up or growing organizations, may benefit more from equity financing or venture capital. Finally, Canadian businesses may also consider government programs that are geared towards providing financial assistance to those meeting certain criteria.

Banks

Banks in Canada are sophisticated and secure. Both domestic chartered banks and foreign banks operate in Canada and are federally regulated by the Bank Act.

Domestic banks include the so-called “big five” that dominate the private financing sector in Canada: The Toronto-Dominion Bank, Canadian Imperial Bank of Commerce, Bank of Montreal, The Bank of Nova Scotia, and Royal Bank of Canada. As of December 2019, there were 37 domestic banks operating Canada.

Foreign banks operate either through subsidiaries or branches, performing banking activities similar to domestic banks, but with certain restrictions. As of December 2019, there were 53 foreign banks operating in Canada either through a subsidiary or a branch. Generally speaking, foreign bank branches must identify as a full service or lending branch, with the former restricted from accepting deposits for less than C$150,000, while the latter are not permitted to accept deposits at all. Thus, foreign banks can be limited in the type of business they can carry on in Canada.

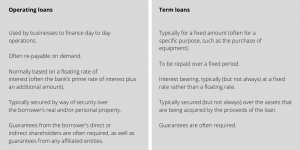

Types of Bank Loans

While there are a multitude of loan types, the two most common types of bank loans are operating loans and term loans. These generally have the attributes as set out below:

Other Sources of Financing

Aside from banks, there are other regulated institutions, as well as unregulated specialty finance companies, that offer financing services to Canadian businesses.

Trust companies

Trust companies are regulated entities similar to banks in that they can take deposits and offer services such as mortgages, loans and investments. Unlike banks, trust companies offer fiduciary services and trust activities, such as managing the assets of a trust.

Credit unions

Credit unions are provincially regulated entities that are also similar to banks as they offer a wide range of financial products and services such as chequing and savings accounts, loans, and credit services. A main differentiator between banks and credit unions is that credit unions operate as not-for-profit entities, which allows them to offer higher saving rates and lower loan rates. Also, credit unions are sometimes less accessible to the general public as they typically only deal with members of the credit union. Membership of a credit union is governed by the credit union’s by-laws, which will require the person or entity to hold a minimum number of membership shares, thus, partially owning the credit union.

Specialty Finance Companies

Largely unregulated, there are also a myriad of specialty lenders, often private corporations, providing a wide range of financing options for Canadian businesses. Among the options these lenders can typically offer are private mortgage loans, equipment leasing facilities, accounts receivable factoring programs, credit lines for inventory acquisition and distribution finance, asset-based loans and purchase order finance programs. The cost of borrowing for these financing options is typically higher than for more traditional options, but the availability and flexibility these options provide can often override the cost and be more attractive to certain businesses.

Equity Financing

Equity can be raised through the sale of shares to the public, however doing so is highly regulated and the costs are quite substantial and beyond the scope of this article. Private placements also allow for the raising of funds from the issuance of private company equity, provided certain rules and regulations are followed – primarily tied to the worth and sophistication of the investor from which funds are obtained. Venture capitalists typically utilise the private placement mechanism to provide financing to corporations, particularly start-up companies, with a view to potentially obtaining large returns on their investments when and if those enterprises conduct a public offering of their equity.

Equity investments generally involve ceding significant control over the management and direction of a company and are thus considered to be the most expensive financing option available.

Government Assistance

Both federal and provincial levels of government have established government assistance programs to assist in financing companies that meet certain criteria. Examples of government programs available in Ontario include the federal Canada Small Business Financing Program (CSBFP) and Community Futures Ontario (CF).

Canada Small Business Financing Program

The program is operated by the Government of Canada and offers support for loans to for-profit businesses in Canada with gross annual revenues under C$10 million. The loans are not available to farming businesses. These loans are available to help finance the purchase or improvement of land or buildings used for commercial purposes, the making of leasehold improvements in leased premises, the purchase of new or used equipment, or the registration fee for the program. The program does not provide financing for things such as goodwill, working capital, inventories, franchise fees, research and development or assets that a holding company acquires.

Loans of up to C$1 million are available under the program, of which no more than C$350,000 can be used to finance the purchase of new equipment or leasehold improvements. The rest of the loan can be used for other business-related purposes as mentioned above. Participants in the program have to pay a registration fee of 2% of the total amount of the loan.

The interest rates for loans under this program can be either variable or fixed. The maximum for a variable rate is the prime lending rate of the lender bank or credit union participating in the program, plus 3%. For a fixed rate, the maximum chargeable is the lenders’ mortgage rate plus 3%. Lenders are required to take security in any assets financed and may also take additional security in the form of personal guarantees.

Community Futures Ontario Program

This is a non-profit program operated by the Community Futures Network of Canada and is aimed at financing start-ups and small businesses in Northern Ontario and rural areas of Southern and Eastern Ontario. It offers business support services for eligible companies, including advice, counselling, information, planning and training. Loans offered through the program are up to C$150,000.

The Business Development Bank of Canada

The Business Development Bank (BDC) is a Crown corporation owned by the federal government and assists small and medium-sized enterprises in Canada. It offers financing and management services for a variety of programs for business, such as start-up financing, purchasing a business, accessing working capital, investing in real estate, purchasing equipment, or expanding a business. BDC offers consulting services as well as financing to its customers. Term financing options offer interest at both fixed and floating rates and schedules for repayment are tailored to the working capital needs of the business borrower. BDC’s approach to risk assessment enables it to assist businesses whose financial needs go beyond the parameters of traditional financing options.

In summary, Ontario offers many varied options to a business for its financing needs, running the gamut from traditional to non-traditional, complex to commonplace. Just as each business can be unique unto itself, so too can available financing solutions be tailored to match a business’s needs at any given time. Understanding the business and the finance options available are the key to arranging an optimal financing program.