Ontario has experienced exponential growth in the recent past. Much of that growth can be attributed to the stable economy associated with a land registration system that emphasizes predictability and the assurance that the records maintained by each land registry office can be relied upon, coupled with a legal planning framework that places an emphasis on new development paying for itself.

These opportunities, with limited exceptions, are available to non-resident investors and owners.

When purchasing and developing property in Ontario, several factors must be considered before a transaction can be completed. Generally, a developer or property purchaser will need to employ a legal team as well as other professionals to advise on obtaining the legal title to the property and title insurance, payment of taxes, and ensuring that the property complies with (or can be made to comply with) planning and zoning requirements and relevant fire and building codes.

Legal Title

Canada’s Constitution allocates legislative authority over private property rights to the provinces. Accordingly, each province has created its own land registry system. There is no land registry at the federal level.

Title to real estate in Ontario was historically registered in one of two paper-based systems, the Registry System and the Land Titles System. In recent years, an electronic title registration system has been established ensuring consistency within the province.

Registration of properties

The Registry Act established the title Registry System in which deeds, mortgages and other documents evidencing an interest in real estate are registered in chronological order.

The Land Titles Act established the Land Titles System that guarantees title to land in favour of the owner reflected in the land records maintained by the province and creates a fund that is available to pay out any person whose interest in the land is found to be inconsistent with the provisions of the title records, subject to a number of exceptions.

In the 1990s, the province embarked upon a project to convert all titles to an electronic format. This ultimately involved not only the electronic registration of property documents but also the electronic execution of such documents. To accommodate the move to electronic registration, most titles in the province were converted to the Land Titles System.

Currently, very few titles remain in the Registry System and, those that do, have not been converted to the Land Titles System by reason of some title issue that must be resolved prior to their conversion into the guaranteed title system.

Title Insurance

Ownership of properties registered in the Land Titles System may still be challenged based on statutory exceptions and the common law.

While undertaking legal due diligence in the acquisition or mortgaging of land and confirming that title will be sufficient to provide a purchaser or lender with good title or security, Ontario lawyers undertake several off-title searches. These include, for example, confirmation that property taxes are not in arrears, that certain statutory easements do not apply to the property, and in the case of condominium units, that the condominium monthly common expenses are fully paid and up to date. Each of these encumbrances run with the title and will therefore be unaffected by a change in ownership or the registration of a mortgage.

In the past 20 years, title insurance has become a standard facet in the acquisition and mortgaging of real estate in Ontario.

Title policies are obtained in the course of a purchase or mortgage transaction, and the insurer will insure certain aspects of title relying on the opinion as to title provided by the lawyer for one of the parties to the transaction. Such policies protect the insured from certain title matters, and other risks such as identity fraud.

A single premium payment paid at the time of the completion of the transaction protects the lender or the owner for the duration of the ownership of the property, or mortgage until it is discharged. A lender and a purchaser will usually discuss the advisability of obtaining title insurance with their lawyer in the course of the transaction. The title insurer will generally not require the lawyer to undertake the full suite of title and off-title examinations (which can be quite expensive) for it to issue the policy.

Tax Matters

Certain taxes such as Land Transfer Tax and HST may be payable on the acquisition of real estate in Ontario.

Land Transfer Tax

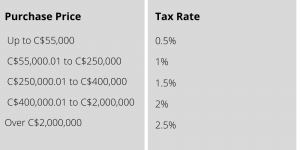

Land Transfer Tax is payable by the purchaser upon the acquisition of an interest in real estate, based on the purchase price of the property and whether the land is residential or non-residential. The residential rate of land transfer tax is as follows:

In addition to the Land Transfer Tax payable by all purchasers in Ontario, the City of Toronto has enacted its own land transfer tax regime, which adds the same amount of tax on property acquisitions within the City of Toronto. First-time home buyers may be entitled to receive a rebate.

Non-Resident Speculation Tax

Home buyers who are not citizens or permanent residents of Canada, or are foreign corporations or trustees, must pay a Non-Resident Speculation Tax (NRST) of 15% for property purchases in the Greater Golden Horseshoe Region. NRST applies to residential property containing up to six single family residences.

Harmonized Sales Tax

Ontario also has a combined provincial tax on the acquisition of real estate that has been harmonized with federal goods and services tax payable under the Excise Tax Act (Canada). This tax is referred to as the Harmonized Sales Tax (HST). Generally, the sale of used residential properties is exempt from HST, but the sale of vacant land by corporations or commercial lands is typically subject to HST.

However, where a purchaser is acquiring the real estate in the course of a commercial activity carried on by it, the purchaser is entitled to claim an input tax credit in the amount of HST that it was required to pay provided that the purchaser is an HST registrant at the time of the sale. Given that the rate of HST in Ontario is a hefty 13%, this is a key consideration in the sale and purchase of real estate in Ontario. The failure of a purchaser to properly classify the acquisition of property as exempt or taxable or to qualify for an input tax credit, or, conversely, the failure of a seller to properly collect HST on a taxable sale, can be serious.

Development

A purchaser of property in Ontario may also need to consider the planning regime in the province in the course of making its purchase decision, where the land is to be subdivided, developed or used for a purpose different from the use of the property on the day of purchase.

Since the 1940s, the rules governing development of land in Ontario, including the creation of new parcels of land by severance or subdivision, have been laid out in several statutes, most importantly, the Planning Act (Ontario). Motivated by the need to coordinate growth, particularly in the urban centres, with the availability of municipally provided services, the Planning Act prohibits the creation of new parcels of land by severance or subdivision without the consent of the municipal government. In some cases, the provincial government’s approval is required.

The Planning Act requires any person who seeks to divide a parcel of land for sale to do so in a manner mandated by the Act. Usually, this means an application to a provincially mandated Land Division Committee that has the authority to approve or refuse an application for a severance to create a new lot.

The creation of numerous new lots must proceed by way of an application for a plan of subdivision, which may likewise be approved or refused. An applicant is entitled to appeal a refusal, or the imposition of unsatisfactory conditions of approval, to a specialized tribunal called the Local Planning Appeal Tribunal, whose decision, except on narrow grounds, is final.

Land Use

The use to which a property may be put is subject to a zoning regime also set out in the Planning Act. If a change in land use is inconsistent with the provisions of the applicable zoning by-law, zoning must be changed by way of a re-zoning application made to the Municipal Council. However, if the non-conformity with the existing zoning is minor in nature, an application for a minor variance to the requirements of the zoning by-law made to the Committee of Adjustment may suffice.

Where the long-term plan for the area in which the property is located is different from the intended use by the purchaser (called the “Official Plan”), the re-zoning application may need to be accompanied by an application to amend the Official Plan. Applications for these amendments are sometimes controversial and may involve a very lengthy process. As with decisions of the Land Division Committee, the ultimate decision of the Municipal Council or the Committee of Adjustment may be appealed to the Local Planning Appeal Tribunal.

Building And Fire Codes

In addition to obtaining the necessary planning approvals, the owner of land will be required to satisfy the technical building requirements of the prevailing Building and Fire Codes in force at the time of submission of the application for a building permit.

Most municipalities have also passed development charge by-laws (and many school boards have passed education development charge by-laws) that require a building permit applicant to pay development charges to be used by the municipality and the school boards to pay a portion of the new municipal and educational infrastructure required as a result of the development. These fees can add a significant cost to the investment as they can amount to many thousands of dollars to be paid by the owner.